What is cooking in Exxaro Tiles Ltd.

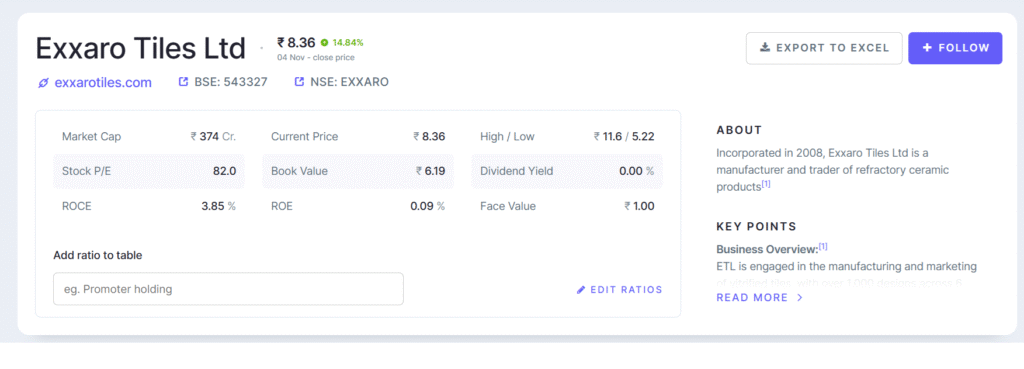

52‑Week Range: ₹5.00 (low) to ₹11.00 (high at listing) (screener).

Current Market Price (CMP): ~₹7–8 (as of Feb 26, 2026).

✅ Positive Signals

- Recent strong quarterly improvement

- In Q4 (March 2025) the company reported revenue of ~ ₹94.98 crore (≈ ₹949.8 m) vs ~₹79.77 crore in Q4 2024: ~19 % YoY growth.

- Net profit in that quarter rose ~193% to ~₹3.51 crore vs ~₹1.20 crore in the prior year quarter.

- Also for December 2024 quarter: sales grew ~21.7% YoY to ~₹79.44 crore and net profit rose ~85% to ₹1.24 crore.

These show the company may be turning around its business momentum.

- Industry tailwinds

- The tile / vitrified-tiles segment has favourable demand drivers: growth in housing, renovations, infrastructure projects, exports.

- Exxaro, with manufacturing bases in Gujarat and product range in vitrified tiles, is positioned to benefit if the market expands.

- Potential operational leverage

- If Exxaro can maintain or improve growth in revenue while controlling costs/margins, there is room for profit improvement from relatively low base.

- With the current profit levels being small in absolute terms, even modest improvement could translate into decent percentage gains.

- Share-market developments

- The stock had earlier proposed a stock-split (1:10) to improve liquidity and awareness. mint

- Improving quarterly numbers may help rebuild investor confidence.

- 🔮 Projection Scenarios for Next 2 Years (FY25 → FY26)

We assume FY25 = year ending March 2025 (or roughly) and FY26 the following year.

| Scenario | Revenue Growth p.a. | Net Margin | FY25 Revenue | FY26 Revenue | FY25 Net Profit | FY26 Net Profit |

|---|---|---|---|---|---|---|

| Moderate | 12% | 1.5% | ~₹3,405 m | ~₹3,813 m | ~₹51 m | ~₹57 m |

| Optimistic | 18% | 2.5% | ~₹3,586 m | ~₹4,232 m | ~₹90 m | ~₹106 m |

| Bull | 25% | 4.0% | ~₹3,799 m | ~₹4,748 m | ~₹152 m | ~₹190 m |

Assumptions & logic:

- Revenue starts from ~₹3,039 m, grows by the indicated % each year.

- Net margin improves over current weak levels (FY24 margin was ~0.7% per one report).

- The “Bull” case expects meaningful margin improvement (via cost efficiency, premium product mix, exports) and strong growth.

- These are illustrative only — actual results may differ.

Implied Valuation & Price-Upside Potential

- Let’s assume the market might value Exxaro at a PE ratio in the range of 30x to 50x (depending on growth & sentiment). Then we estimate implied market cap & share-price potential.

- If net profit = ₹90 m (Optimistic FY25) and PE = 40x → market cap ~ ₹3,600 m.

- If net profit = ₹152 m (Bull FY25) and PE = 50x → market cap ~ ₹7,600 m.

- Current market cap (approx) ~ ₹3,000-4,000 m (based on revenue and stock price data) so in bull scenario the market cap could ≈2x.

- If both growth and margin accelerate further into FY26 (₹190 m profit) and PE expands to say 50x → market cap ~ ₹9,500 m → ~3x potential.

- Hence, under favourable execution you could see doubling to tripling of valuation over 1-2 years — but this is contingent on growth + margin expansion + market re-rating.

Key Triggers for the Upside

- For these scenarios to play out, Exxaro will likely need:

- Sustained revenue growth in the double digits (15-25 %) not just one quarter.

- Margin improvement: moving from sub-1% net margin to perhaps 2-4% or more.

- Expansion of premium product mix, export growth, better utilisation of capacity.

- Improvement in cash flows, working capital, reduction of debt and higher returns on capital.

- Positive market sentiment and a re-rating (investors willing to give higher PE).